Ideas

"Fertilizer companies are moving higher after having a very good day yesterday... because the Strait of Hormuz isn't just a chokepoint for energy but also fertilizers. In Turkey some of their fertilizers have curbed exports." The Middle East is a major exporter of global fertilizer components. With the Strait of Hormuz blocked and regional players hoarding supply, global agricultural input prices will spike. North American producers will benefit from immense pricing power and margin expansion without facing the same logistical blockades. LONG. The supply chain shock provides a direct catalyst for domestic fertilizer producers to capture global market share at premium prices. Demand destruction if farmers refuse to plant at higher input costs, or a rapid reopening of global shipping lanes.

"The real yield is high enough now to be covering what we think the longer run equity policy rate probably is... To an investor entering into real yield close to two, that seems like a great opportunity and I think that the people will be purchasing TIPS here because they like the real yield and are thinking that inflation could rise." The oil shock is shifting the macro narrative from disinflation to stagflation. Treasury Inflation-Protected Securities (TIPS) offer a dual benefit right now: locking in historically attractive absolute real yields (~2%) while providing a direct hedge against the headline CPI spikes that will inevitably follow $100+ crude oil. LONG. TIPS provide a mathematically sound safe haven that compensates investors for both duration risk and upward inflation surprises. If the geopolitical conflict resolves quickly, oil prices will crash, dragging down inflation expectations and the principal value of TIPS.

"If that is the case, all of the sudden with Iran, hyperscalers and AI trade is now looking like a quality trade again because they are more insulated from what is happening geopolitically. I think there will be more flows into those companies." While rising energy costs are a headwind for data centers, hyperscalers have fortress balance sheets and massive cash reserves. In a stagflationary or geopolitically unstable environment, investors will flee cyclical sectors and hide in mega-cap tech, treating them as safe-haven assets that can self-fund their growth regardless of macro conditions. LONG. Hyperscalers offer a rare combination of secular growth (AI) and defensive balance sheet quality during a global supply chain crisis. A severe stagflationary recession could force enterprise customers to slash the cloud and software budgets that drive hyperscaler revenues.

"Jefferies lowering its price target on Delta, noting the steep rise in jet fuel prices... Air France raising the long haul ticket prices because of the cost of oil." Airlines are highly sensitive to energy input costs. To protect margins from spiking jet fuel, airlines must raise ticket prices (estimated 8-9% increases). This will cause immediate demand destruction among consumers who are already squeezed by higher inflation and gasoline prices, leading to downward earnings revisions. SHORT. The airline sector is caught in a stagflationary trap of rising operating costs and deteriorating consumer discretionary spending power. A swift drop in oil prices or stronger-than-expected consumer willingness to absorb higher ticket prices for travel.

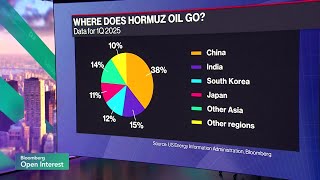

"Wells Fargo doubly upgrading Occidental to overweight. Finally Piper Sandler raising its price target on Exxon. The analyst revising estimates on the back of higher crude." The closure of the Strait of Hormuz is creating a massive physical supply deficit that strategic reserve releases cannot fix. Domestic US oil producers are completely insulated from Middle East shipping chokepoints and will capture massive free cash flow windfalls from sustained $90-$100+ crude prices. LONG. Upgrades and price target hikes reflect the immediate earnings translation of the geopolitical risk premium into domestic energy equities. A sudden diplomatic resolution or ceasefire in the Middle East would rapidly collapse the geopolitical risk premium in crude oil.

"The private credit problems are likely to continue... The real question is what is the impact to the banks. The banks have exposure to private credit players but this is nothing like what we saw in 2008 or 2009... They have been so de-risked since the financial crisis they will be able to weather any storm that comes from private credit." The market is indiscriminately punishing the broader financial sector due to headlines about private credit funds gating redemptions. However, large depository banks are heavily regulated, over-capitalized, and lack direct exposure to the riskiest private loans, creating a mispricing opportunity to buy high-quality bank stocks on unwarranted contagion fears. LONG. Large-cap banks are a buy as they will survive the private credit shakeout and potentially gain market share as shadow banking retreats. If oil stays above $100 for 12 months, it could trigger a severe consumer recession, leading to broad credit card and auto loan defaults that would hurt traditional banks.

"Morgan Stanley, its BDC on North Haven would be gating redemptions at 5% for its private credit fund, feeding into fears over the funds themselves and private credit. Shares down 2.8% of Morgan Stanley in the premarket trade." Alternative asset managers and banks with large retail-facing private credit vehicles are facing a liquidity mismatch. As investors panic and demand cash, these funds are forced to gate redemptions, which damages their reputation, halts new capital inflows, and threatens the lucrative fee streams that have driven their stock valuations. AVOID. The opacity of private credit marks and the gating of funds will create a sustained overhang on the stock prices of the sponsoring institutions. If the Federal Reserve unexpectedly slashes interest rates, it could inject enough liquidity into the system to bail out private credit borrowers and stop the redemption wave.

This Bloomberg Markets video, published March 12, 2026,

features Dani Burger, Stephen Major, Austin Quan, Jonathan Ferro, Gerard Cassidy

discussing MOS, CF, TIP, MSFT, META, GOOGL, AMZN, DAL, XOM, OXY, WFC, BAC, C, JPM, MS.

7 trade ideas extracted by AI with direction and confidence scoring.

Speakers:

Dani Burger,

Stephen Major,

Austin Quan,

Jonathan Ferro,

Gerard Cassidy

· Tickers:

MOS,

CF,

TIP,

MSFT,

META,

GOOGL,

AMZN,

DAL,

XOM,

OXY,

WFC,

BAC,

C,

JPM,

MS