Oil Prices Are Rising Fast… Is a Global Recession Next? w/ Peter St Onge

Speakers

John Gillen

— Co-Host, Milk Road Macro

Peter St. Onge

— PhD Economist & Senior Fellow, Heritage Foundation

Summary

- A US recession triggered by oil prices requires a sustainable doubling of the price (to roughly $135/barrel); the current $20 jump to ~$86 only shaves an estimated 0.5% off GDP and is not catastrophic.

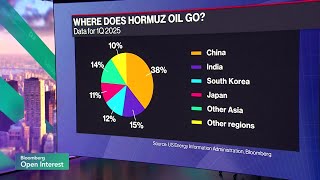

- The US and Europe are largely insulated from Middle East oil shortages due to strategic reserves and domestic drilling, whereas Asia (China, India, Japan, Korea) is highly exposed and vulnerable to supply shocks.

- China's economy is in a precarious state, facing its lowest growth in 35 years, a massive property bust, and severe manufacturing overcapacity, giving the US significant leverage in ongoing trade negotiations.

- AI is not causing aggregate job losses yet, but it is severely impacting entry-level white-collar hiring (tech hires are down 25%). Conversely, blue-collar jobs remain insulated and are poised to benefit from AI-driven wealth creation.

- In the AI investment landscape, hardware and semiconductor companies have clear economic moats, whereas SaaS and software applications are highly vulnerable to AI disruption eroding their barriers to entry.

Ideas

"For this year I'm very bullish on the sort of picks and shovels in AI that means overwhelming semis. So, Nvidia, Broadcom, companies like that." AI applications currently lack clear economic moats, making it difficult to pick software winners. However, the massive venture capital flowing into AI development guarantees immediate and sustained revenue for the hardware and semiconductor companies building the underlying infrastructure. LONG. "Picks and shovels" (semiconductors) are the safest, most profitable way to play the AI boom while the software landscape remains unsettled. A broader macroeconomic recession or a sudden halt in AI venture capital funding could reduce aggregate demand for high-end chips.

"I don't touch the AI applications and the reason is that I don't know what the MOT's going to be... somebody like Palantir... I wouldn't buy... if you can vibe code Adobe Acrobat in 45 minutes with zero technical training then why is Adobe worth 100 billion?" Generative AI makes coding and software creation exponentially faster and cheaper. This destroys the traditional barriers to entry (moats) for SaaS companies, meaning their current high valuation multiples are unjustified if competitors or users can easily replicate their core products using AI. AVOID. Software and SaaS companies face existential threats to their moats and pricing power due to AI code generation. These companies successfully integrate AI into their proprietary ecosystems, locking in enterprise customers and justifying their high multiples through distribution rather than pure tech.

"Usually I think it's prudent to keep a batch of money in you know like the mag 7 and you know companies like Google or something Amazon... [but] to the extent their mode is based on software could be vulnerable to AI." Mega-cap tech stocks have historically been safe havens with massive, impenetrable moats. However, because their core businesses rely heavily on software ecosystems, they are not entirely immune to the disruptive, moat-eroding effects of AI, requiring investors to monitor them closely rather than blindly holding them as risk-free assets. WATCH. While traditionally safe, their software-centric moats need to be continuously re-evaluated in the age of generative AI. They may simply acquire emerging AI threats or use their massive distribution and compute advantages to crush open-source competitors.

"If you want to make a trade so that you're hedging... you would of course get into energy because oil prices are a proxy for how long the war lasts... Trump has been acquiring stakes in various companies to try to get them to up production. So for example, rare earths I think uranium lithium." If the Middle East conflict extends past the expected April timeline, global supply chains will be strained, driving up oil prices. Additionally, political moves to secure domestic production of strategic commodities will benefit uranium and lithium assets as the US pivots away from reliance on foreign adversaries. WATCH. These are defensive hedges to deploy only if the geopolitical situation deteriorates and the war timeline extends longer than the market currently prices in. The war ends quickly (as the speaker predicts), causing a rapid unwinding of geopolitical risk premiums in energy and strategic commodities.