Ideas

The Trump administration is drafting regulations requiring US approval for *all* exports of AI accelerators (specifically naming Nvidia and AMD) to *anywhere in the world*, not just China. This moves from a "China restriction" to a "Global restriction." It introduces massive friction, bureaucratic delays, and potential denials for sales to the Middle East, Southeast Asia, and other markets. This effectively shrinks the Total Addressable Market (TAM) and adds regulatory overhead. Short US AI chip designers as the geopolitical fence tightens around their revenue streams. The regulations could be watered down before implementation; AI demand is so high that buyers may tolerate the delays.

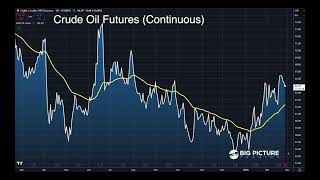

Goldman Sachs raised their Q2 Brent forecast by $10/bbl to $76. Dart notes that if flows through the Strait of Hormuz remain low for "another five weeks," prices could cross the $100/bbl threshold. While the US administration is trying to engineer lower prices (waivers, SPR talk), the physical reality of a supply disruption in the Strait creates an asymmetric upside risk for oil prices. The "war premium" is back. Long exposure to crude oil futures or energy producers. US Treasury intervention or a rapid de-escalation of the conflict leading to a price collapse.

Hong Kong Land CEO states vacancy in their Central portfolio has dropped to 6% (market rents are inclining). He explicitly mentions a "capital markets led" recovery with demand from hedge funds and family offices. The narrative on Hong Kong commercial real estate has been overwhelmingly bearish. If the premier landlord in the Central district is seeing positive reversions and falling vacancy, the stock is likely mispriced against peak pessimism. Long the ADR for Hong Kong Land as a contrarian play on HK financial activity recovery. Broader geopolitical tensions involving China/HK; global financial slowdown reducing office demand.

JD.com reported its first quarterly loss in four years due to intense competition in food delivery. Mainland investors sold a record amount of Hong Kong shares in a single session, rotating out of internet stocks. The "platform economy" in China is suffering from a price war (deflationary pressure) and regulatory fatigue. Capital is fleeing these names to chase state-sanctioned "hard tech" (semiconductors) instead. The fundamental earnings power of the internet giants is eroding. Avoid or Short Chinese internet majors. A sudden stimulus package from Beijing specifically targeting consumer spending could trigger a short squeeze.

South Korea and Taiwan rely heavily on LNG from the Gulf (Qatar/UAE). Taiwan has phased out nuclear and restricted utility-scale solar; Korea has limited storage (less than 2 months). These economies are the "chip fabs" of the world but have fragile power grids. A prolonged disruption in the Strait of Hormuz threatens their energy security more acutely than other nations, creating systemic risk for their broader equity markets. Short South Korea (EWY) and Taiwan (EWT) ETFs as a hedge against energy insecurity. The conflict resolves quickly, restoring normal LNG shipping routes.

Oracle is planning to cut thousands of jobs to handle a "cash crunch" resulting from a massive data center expansion effort. While expansion indicates demand, the phrase "cash crunch" is a red flag for liquidity and capital management. It suggests they are overextended and forced to cut OpEx (jobs) to fund CapEx, which can signal operational distress. Short/Watch Oracle on signs of liquidity stress. The market may interpret the job cuts as "efficiency" and reward the stock for margin improvement.

This Bloomberg Markets video, published March 06, 2026,

features Brendan Fagan, Samantha Dart, Michael Smith, Charlotte Yang, David Fickling, News Anchor (Text Scroll/Voiceover)

discussing NVDA, AMD, XLE, USO, HNGKY, JD, BABA, TCEHY, EWY, EWT, ORCL.

6 trade ideas extracted by AI with direction and confidence scoring.

Speakers:

Brendan Fagan,

Samantha Dart,

Michael Smith,

Charlotte Yang,

David Fickling,

News Anchor (Text Scroll/Voiceover)

· Tickers:

NVDA,

AMD,

XLE,

USO,

HNGKY,

JD,

BABA,

TCEHY,

EWY,

EWT,

ORCL