Ideas

The "squeezed middle" retailers are in "no man's land." Store closures and rightsizing are ongoing. These retailers lack the pricing power of luxury and the value proposition of discounters. Rising gas prices will further deter their core consumer base. AVOID Department Stores. Potential M&A activity or privatization bids.

Reports indicate the US is weighing capping the number of AI accelerators Nvidia can export to China (limit of 75,000 H200 chips per firm). Geopolitical tensions are bleeding into trade policy. Capping sales to a major growth market restricts revenue potential for high-flying chipmakers, adding regulatory risk to the valuation. AVOID / NEUTRAL on AI Hardware exposed to China export controls. The caps may not be implemented, or demand elsewhere (US hyperscalers) may absorb the supply.

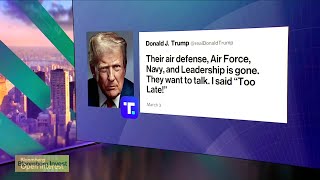

Brent Crude broke $85. Qatar Energy halted LNG output. 20% of global energy supply is at risk due to the Strait of Hormuz closure. "Battalion Energy" (BATL) is explicitly mentioned as up ~127% tracking oil. The market is repricing a structural risk premium into energy. Unlike 2022, US producers are insulated from the physical blockade but benefit from global price spikes. Verrone notes Energy leadership predates the war, confirming a structural trend. LONG US-based energy producers and the broad sector. Rapid de-escalation or release of Strategic Petroleum Reserves (SPR) dampening prices.

Target (TGT) earnings beat with positive outlook (shares +4%). Consumers are spending on necessities; Costco (COST) and Walmart (WMT) are gaining market share. In an inflationary/uncertain environment (rising gas prices), consumers trade down to value. Retailers with scale and efficiency (Walmart/Costco) or off-price models (TJX) win share from the "squeezed middle." LONG Value & Efficiency Retailers. Supply chain disruptions (shipping costs) eating into margins.

European Natural Gas prices are up ~80% in 48 hours. The DAX is down ~4%, Italian equities down ~5%. Europe is heavily dependent on imported LNG (specifically Qatar). Europe faces a "2022 Volume 2" energy shock. Unlike the US, Europe lacks domestic energy production and AI/Tech giants to offset the drag. This is a pure stagflationary hit to the Eurozone economy. SHORT European Equities (Broad Europe, Germany, Italy). Fiscal intervention by EU governments to subsidize energy costs.

Japanese markets sold off heavily (correlated with global risk-off). Verrone argues the structural bull case for Japan (corporate reform, robotics, industrials) remains intact. The sell-off is an emotional reaction, creating an entry point for "oversold conditions." LONG Japanese Equities (Buy the dip). Continued global contagion or Yen volatility.

12,000 flights canceled globally. Oil prices spiking (Jet Fuel costs). Airlines face a "double whammy": rising operational costs (fuel) and lost revenue (cancellations/fear of travel). Margins will be crushed. SHORT Airlines. Government support or oil price collapse.

Despite a major war, Gold is not making new highs and Silver reversed 15% lower. "Price First" philosophy: If an asset cannot rally on the exact news it is theoretically designed for (war/fear), the bull market is exhausted or broken. The price action contradicts the thesis. AVOID Precious Metals. The market realizes the inflation risk later and rotates back into metals.

Strait of Hormuz closed. Red Sea disrupted. Ocean carriers pausing bookings. Rumors of rates hitting $5,000/container (doubling). A "war on logistics" creates scarcity in shipping capacity. When capacity is constrained and routes are lengthened (avoiding conflict zones), shipping rates spike, directly boosting profitability for liners. LONG Container Shipping. Rapid resolution of conflict reopening shipping lanes.

This Bloomberg Markets video, published March 03, 2026,

features Stacey Widlitz, Annmarie Hordern, Chris Verrone, Torsten Slok, Ryan Petersen

discussing M, KSS, NVDA, AMD, XLE, CVX, BATL, XOM, TJX, TGT, COST, WMT, EWG, EWI, VGK, DXJ, EWJ, JETS, UAL, DAL, SLV, GLD, ZIM, AMKBY.

9 trade ideas extracted by AI with direction and confidence scoring.

Speakers:

Stacey Widlitz,

Annmarie Hordern,

Chris Verrone,

Torsten Slok,

Ryan Petersen

· Tickers:

M,

KSS,

NVDA,

AMD,

XLE,

CVX,

BATL,

XOM,

TJX,

TGT,

COST,

WMT,

EWG,

EWI,

VGK,

DXJ,

EWJ,

JETS,

UAL,

DAL,

SLV,

GLD,

ZIM,

AMKBY